According to the 2025 Lease End Lease Buyout Report, these are the top vehicles that owners commonly buy out of their leases, ranked by the average equity retained by the buyer. The figures the dealership will offer you aren't likely to be an exact match with what you see here, but if you are leasing one of these models, it is more likely to be a great candidate for selling it and making a profit. Similarly, if you choose to buy out your lease, these models are likely to hold their value for longer than others.

Honda Accord ($8,730)

Toyota RAV4 ($8.557)

Honda CR-V ($8,411)

Honda Civic ($7,766)

Toyota Highlander ($6,979)

Toyota Tacoma ($6,897)

Ram 1500 ($6,505)

Honda HR-V ($6,032)

Jeep Grand Cherokee ($6,025)

Jeep Wrangler ($2,901)

This strategy isn't quite available to everyone. A number of automotive finance arms do not allow a third-party buyout of a leased vehicle. The list has grown in recent years, as dealerships that often relied on lease returns to stock their used car inventory now find themselves in serious need of cars to fill their lots and showrooms. In other words, you could have your vehicle appraised on Edmunds to get an independent quote on its value, which is a valuable resource, but you would not be able to redeem the offer at one of our participating dealerships. In this scenario, the remaining options would be to take your vehicle to any dealership of the same brand and get an offer for it or else purchase it from the lease company directly.

We try to keep this list up to date, but rules are constantly changing. Please double-check with your leasing company to know your options. Note that in some of the restricted cases below, a third-party buyout may be allowed if the buyer is a dealership, not an individual. So be sure to read the fine print to be fully clear on your options.

Auto finance companies that have partial or complete restrictions on third-party off-lease buyouts:

Source: CarMax

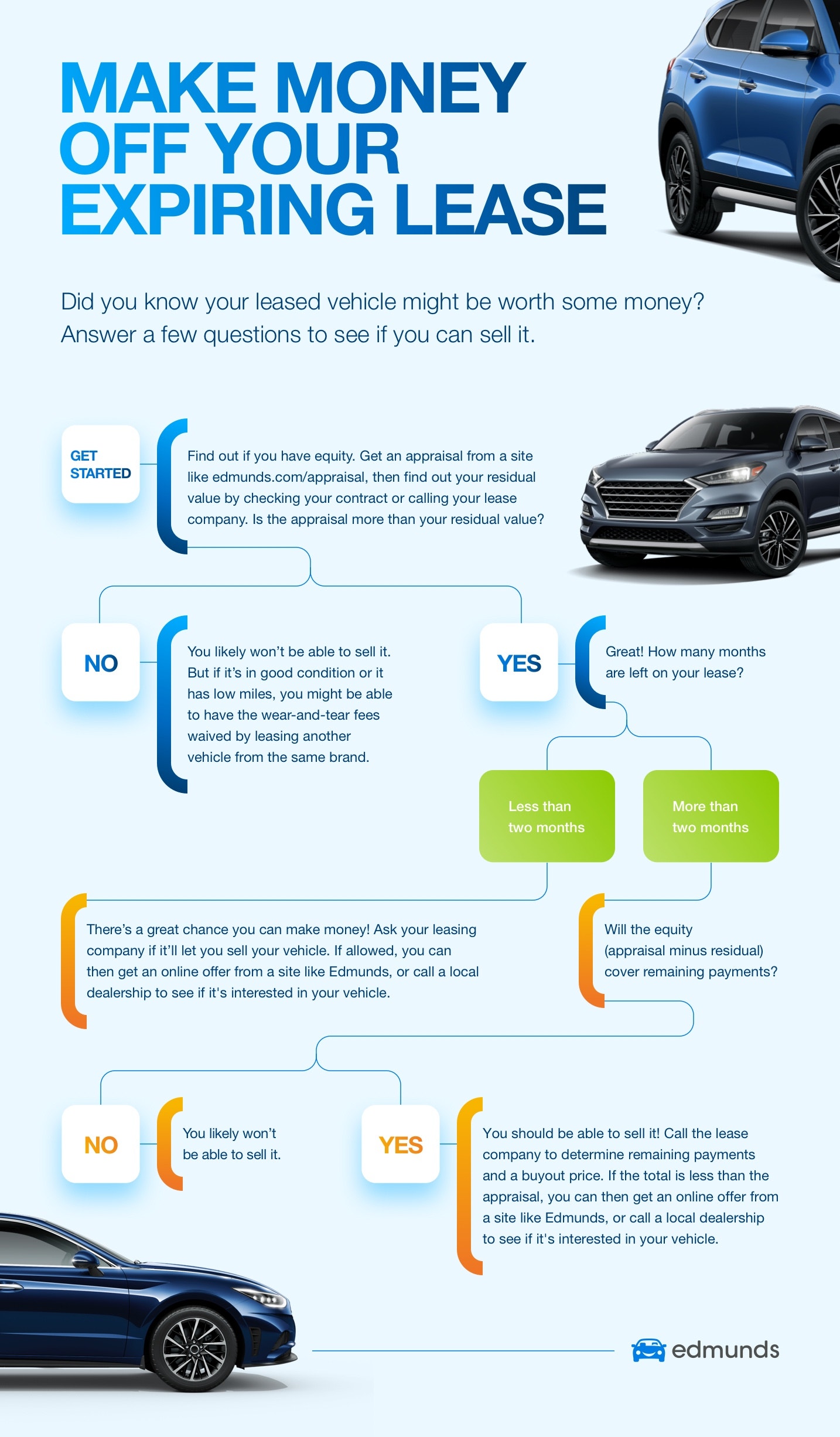

You'll need an appraisal to determine if you have positive equity. Just enter a few details about your vehicle and soon you'll have a price for your vehicle that can be paid out that same day. Not all leased vehicles have equity, of course. But as your lease return date draws near, keep an eye on its market value. Keep in mind, though, that these strategies may not apply to everyone:

1. Sell your leased car and get a check.

Assuming your leased car isn't from the prohibited brands above, you can take your car to any dealership, not just the one where you arranged the lease. The dealership will buy the car at the trade-in price, then arrange to pay the leasing company what you owe and give you a check for the equity. However, don't expect the money immediately in this scenario. The dealership will mail you a check once it gets a clear title, assuring that your car doesn't have any outstanding parking tickets. Just in case, ask to get the trade-in agreement in writing and state the amount due to you.

Can you sell a leased car to CarMax*?

Yes, in fact, we highly recommend it. According to the company, you can sell your leased vehicle to CarMax in almost the same way as any other financed car. It will appraise the car or truck, then contact the leasing company for a payoff quote and process any equity you might have. You can get the process started on Edmunds with an appraisal, which will give you an offer from CarMax, plus a few other dealerships. The CarMax offer is good for seven days and redeemable at any of their locations. Enter a few details about your vehicle, and you'll soon have a price for it that can be paid out that same day. The same applies to heading directly to a CarMax location. (*Disclaimer: Edmunds is owned by CarMax, but we stand by the recommendation.)

2. Sell your leased car to a neighbor, friend or family member. This method requires a bit of trust, so it helps to sell your car to someone you know. But you can sell to any buyer you find, and you'll be able to get the private-party price for the car, which is higher than the trade-in price that dealers pay.

Here's what you do: After finding a trusted buyer, have that person mail a check for the buyout amount to the leasing company. Once you receive the title (the leasing company will only send it to the person leasing the car), sign it to release your interest in the vehicle, and give the title to the buyer. The buyer can then register the car and pay sales tax at that time. But be careful: If the buyer waits longer than 10 days, the state might try to charge you both sales tax, which would wipe out your profit.

According to the Auto Club of Southern California, a way to prevent this situation is to pay the sales tax and DMV fees as soon as possible and then return to the DMV to conclude the deal with the title in hand. This transaction is called a "lease buyout transfer." Contact your state's DMV for more details.

3. Use the equity as the down payment on your next car. In this scenario, the equity in your current car becomes a cash down payment for the new one. Once you know you have equity, you can take your car to any dealer to begin a new lease or sales contract. Not all dealers will offer you the same amount for your leased car buyout, so you might have to shop around for the best offer. The amount should be close to or better than the Edmunds trade-in price.

Dianne Whitmire, fleet and internet director for West Coast Toyota in Long Beach, California, said she uses the equity in returning lease cars to help her customers in a variety of ways. She had one customer with two cars — one was a leased vehicle with equity and one a purchased car that was "upside down," meaning that the loan balance was greater than the car was worth. "In that case, one washes the other" to pay off the loan, she explains. Experts say you might get more money if you are going "brand to brand," meaning selling a Toyota to a Toyota dealership, although any dealership can handle the transaction.

It's important to make sure all the numbers add up. Agree on the exact amount of equity you will receive and look for that amount in the down payment box on the contract. Alternatively, you can also use the equity to pay the fees required to begin a new lease rather than pay that money out of pocket. Finally, if you live in a state that allows a trade-in vehicle to reduce the sales tax, you might want to chat with the dealership to see what the best option is.

Is it a good idea to sell a leased car?

It might be a good idea to sell a leased car before the lease is up if the car is worth more than the residual value that was calculated at the time it was initially leased. If there’s no additional value to gain, it may be a better idea to turn the lease vehicle back in when the leasing period has ended.

Can I sell my car if it is leased?

It may be possible to sell your car if it is leased. Not all auto finance companies allow lessees to sell their leased cars to third parties. If that's the case with the car you are currently leasing, you might need to check your options at a dealership that handles the brand of car you’re leasing.

Can you sell a leased car before the lease is up?

It is possible to sell a leased car before the lease is up, but the early timeframe will vary depending on the leasing company. For example, some companies allow a sale six months before the lease is up, while others allow it only a month before the lease expires. You are responsible for the remaining payments on the lease, so take that into consideration because that remaining balance might cut into the potential profit.

Are leased cars good to buy?

Buying a leased car is a good idea for those looking to break the cycle of leasing and get into a used car. You're the original owner, so need to look into the vehicle's history or do any research on whether you like the car. The price may not be negotiable, so make sure you focus your efforts on determining whether the buyout price is fair.

What is an off-lease car?

An off-lease car is an industry term for a vehicle whose lease has expired and is now being sold as a used car. Many certified pre-owned vehicles are off-lease cars since they are a few years old and have relatively low miles.

What is the cheapest car to lease?

The cheapest car to lease would likely be the base model of a subcompact vehicle. But in general, a lease can be configured to have as low a payment as you'd like provided you make a large enough down payment. The key is to strike a balance between a low monthly payment and a low down payment. Edmunds maintains a list of Best Car, Truck and SUV Lease Deals Under $299. Read it for more information on cheap leasing options.

" fill-opacity=".3" d="M0-111h1200v397s-252.211 51.289-538.449 54C375.312 342.711 0 292 0 292v-403Z"/%3E%3Cpath fill="url(%23b)" d="M1-114h1199v378s-252 51.289-538 54C376 320.711 0 270 0 270v-384Z"/%3E%3Cpath fill="url(%23c)" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3Cpath fill="url(%23d)" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3Cmask id="e" width="1201" height="255" x="-1" y="60" maskUnits="userSpaceOnUse" style="mask-type:alpha"%3E%3Cpath fill="%23EEF1F6" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3C/mask%3E%3Cg mask="url(%23e)"%3E%3Cmask id="g" width="1438" height="328" x="-124" y="-13" maskUnits="userSpaceOnUse" style="mask-type:alpha"%3E%3Cpath fill="url(%23f)" fill-rule="evenodd" d="M-123.5 258.5-109-13h1395l27.5 245c-232.5 34.5-487.705 80.384-725.581 83-237.486-2.721-265.419-4-711.419-56.5Z" clip-rule="evenodd"/%3E%3C/mask%3E%3Cg mask="url(%23g)"%3E%3Cpath fill="%23FEF3C7" fill-opacity=".05" d="M774.502 1161.55c72.001-3.83 144.529-16.6 217.321-38.74C1514.56 964.017 1919.92 369.717 2099-392.74 1846.08 72.142 1341.28 313.096 774.502 323.314 207.726 312.671-296.808 72.141-549.998-392.74-370.919 369.717 34.449 964.017 557.181 1122.81c72.792 21.71 145.32 34.48 217.321 38.74Z"/%3E%3Cpath fill="%232070E8" fill-opacity=".25" d="M1243.34 184.225c102.44 30.548 204.48 74.055 305.68 131.036C2275.79 724.198 2778.24 1714.59 2935.35 2866.48 2634.05 2114.1 1943.59 1594 1134.58 1382.03 322.864 1199.88-429.69 1367.89-852 1944.02-497.039 916.86 159.636 208.787 927.603 163.907c106.887-5.677 212.247 1.329 315.737 20.318Z"/%3E%3Cpath fill="%23FEF3C7" fill-opacity=".05" d="M1232.5 70.76c104.07 5.535 208.91 23.986 314.13 55.967C2302.21 356.131 2888.15 1214.7 3147 2316.21 2781.41 1644.6 2051.75 1296.5 1232.5 1281.74 413.251 1297.12-316.027 1644.6-682.001 2316.21-423.151 1214.7 162.788 356.131 918.372 126.727 1023.59 95.361 1128.43 76.91 1232.5 70.76Z"/%3E%3Cpath fill="%23154A99" fill-opacity=".29" d="M421.155 420.269c113.733 46.994 226.413 108.503 337.53 185.053C1556.67 1154.75 2075.77 2329.98 2199.28 3644.03 1895.3 2761.18 1143.24 2091.29 243.733 1753.08c-903.919-305.05-1757.473-209.22-2258.663 386.12C-1568.66 1028.61-797.982 313.945 67.226 358.413c120.398 6.829 238.484 27.723 353.929 61.856Z"/%3E%3C/g%3E%3C/g%3E%3Cdefs%3E%3ClinearGradient id="a" x1="600" x2="600" y1="-92" y2="449" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".336" stop-color="%23007EE5"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3ClinearGradient id="b" x1="600.5" x2="600.5" y1="-114" y2="427" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".336" stop-color="%23007EE5"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3ClinearGradient id="c" x1="647" x2="647" y1="60" y2="319" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".052" stop-color="%23007EE5"/%3E%3Cstop offset=".514" stop-color="%231561D4"/%3E%3Cstop offset=".938" stop-color="%2300A0B5"/%3E%3C/linearGradient%3E%3ClinearGradient id="d" x1="647" x2="647" y1="60" y2="319" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".282" stop-color="%23007EE5" stop-opacity="0"/%3E%3Cstop offset=".822" stop-opacity=".3"/%3E%3C/linearGradient%3E%3ClinearGradient id="f" x1="588.5" x2="588.5" y1="-13" y2="499.532" gradientUnits="userSpaceOnUse"%3E%3Cstop stop-color="%23154A99"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3C/defs%3E%3C/svg%3E)