" fill-opacity=".3" d="M0-111h1200v397s-252.211 51.289-538.449 54C375.312 342.711 0 292 0 292v-403Z"/%3E%3Cpath fill="url(%23b)" d="M1-114h1199v378s-252 51.289-538 54C376 320.711 0 270 0 270v-384Z"/%3E%3Cpath fill="url(%23c)" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3Cpath fill="url(%23d)" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3Cmask id="e" width="1201" height="255" x="-1" y="60" maskUnits="userSpaceOnUse" style="mask-type:alpha"%3E%3Cpath fill="%23EEF1F6" d="M0 60h1200v188s-327 63.289-613 66C301 316.711 0 273 0 273V60Z"/%3E%3C/mask%3E%3Cg mask="url(%23e)"%3E%3Cmask id="g" width="1438" height="328" x="-124" y="-13" maskUnits="userSpaceOnUse" style="mask-type:alpha"%3E%3Cpath fill="url(%23f)" fill-rule="evenodd" d="M-123.5 258.5-109-13h1395l27.5 245c-232.5 34.5-487.705 80.384-725.581 83-237.486-2.721-265.419-4-711.419-56.5Z" clip-rule="evenodd"/%3E%3C/mask%3E%3Cg mask="url(%23g)"%3E%3Cpath fill="%23FEF3C7" fill-opacity=".05" d="M774.502 1161.55c72.001-3.83 144.529-16.6 217.321-38.74C1514.56 964.017 1919.92 369.717 2099-392.74 1846.08 72.142 1341.28 313.096 774.502 323.314 207.726 312.671-296.808 72.141-549.998-392.74-370.919 369.717 34.449 964.017 557.181 1122.81c72.792 21.71 145.32 34.48 217.321 38.74Z"/%3E%3Cpath fill="%232070E8" fill-opacity=".25" d="M1243.34 184.225c102.44 30.548 204.48 74.055 305.68 131.036C2275.79 724.198 2778.24 1714.59 2935.35 2866.48 2634.05 2114.1 1943.59 1594 1134.58 1382.03 322.864 1199.88-429.69 1367.89-852 1944.02-497.039 916.86 159.636 208.787 927.603 163.907c106.887-5.677 212.247 1.329 315.737 20.318Z"/%3E%3Cpath fill="%23FEF3C7" fill-opacity=".05" d="M1232.5 70.76c104.07 5.535 208.91 23.986 314.13 55.967C2302.21 356.131 2888.15 1214.7 3147 2316.21 2781.41 1644.6 2051.75 1296.5 1232.5 1281.74 413.251 1297.12-316.027 1644.6-682.001 2316.21-423.151 1214.7 162.788 356.131 918.372 126.727 1023.59 95.361 1128.43 76.91 1232.5 70.76Z"/%3E%3Cpath fill="%23154A99" fill-opacity=".29" d="M421.155 420.269c113.733 46.994 226.413 108.503 337.53 185.053C1556.67 1154.75 2075.77 2329.98 2199.28 3644.03 1895.3 2761.18 1143.24 2091.29 243.733 1753.08c-903.919-305.05-1757.473-209.22-2258.663 386.12C-1568.66 1028.61-797.982 313.945 67.226 358.413c120.398 6.829 238.484 27.723 353.929 61.856Z"/%3E%3C/g%3E%3C/g%3E%3Cdefs%3E%3ClinearGradient id="a" x1="600" x2="600" y1="-92" y2="449" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".336" stop-color="%23007EE5"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3ClinearGradient id="b" x1="600.5" x2="600.5" y1="-114" y2="427" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".336" stop-color="%23007EE5"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3ClinearGradient id="c" x1="647" x2="647" y1="60" y2="319" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".052" stop-color="%23007EE5"/%3E%3Cstop offset=".514" stop-color="%231561D4"/%3E%3Cstop offset=".938" stop-color="%2300A0B5"/%3E%3C/linearGradient%3E%3ClinearGradient id="d" x1="647" x2="647" y1="60" y2="319" gradientUnits="userSpaceOnUse"%3E%3Cstop offset=".282" stop-color="%23007EE5" stop-opacity="0"/%3E%3Cstop offset=".822" stop-opacity=".3"/%3E%3C/linearGradient%3E%3ClinearGradient id="f" x1="588.5" x2="588.5" y1="-13" y2="499.532" gradientUnits="userSpaceOnUse"%3E%3Cstop stop-color="%23154A99"/%3E%3Cstop offset="1" stop-color="%2363D9EA"/%3E%3C/linearGradient%3E%3C/defs%3E%3C/svg%3E)

Do you have bad credit? Brand-new credit? If you do, getting a decent car loan can be tough. The good news is that with some guidance and a little patience, it should be possible to secure a fair car loan regardless of your credit situation.

- 9/12/2018

Here are nine tips that will address your bad credit and help you get into a new ride:

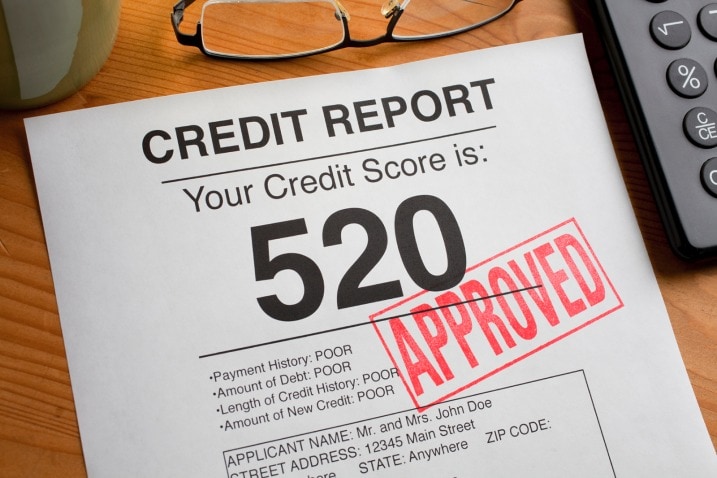

1: Prep Early and Know Your Credit Score

You should start with your credit report to see how it would look to a lender. Run it at least three months before you plan on buying so you can take action on any outstanding items, recommends Rod Griffin, director of public education for credit reporting company Experian.

Annual Credit Report.com gives you one free report a year from each of the major credit bureaus:Experian,Equifax andTransUnion. Take advantage of it. Do your best to pay off any credit cards or outstanding loans. Or at least make a payment to show positive activity on the account.

Many credit card companies offer credit monitoring services to their customers. Mobile apps from Credit Karma, Mint and Experian will also show your credit score if you've signed up for their service.

Once you get the free credit report, pay close attention to the section that points out potentially negative items, also called risk factors. Risk factors could be anything from an old debt that went to collections to a fine you had to pay in a civil court case.

Rather than viewing them as blemishes on your credit, "these risk factors can empower you as a consumer to help rehabilitate your credit," Griffin says. The risk factors are present in all reports, so if you fix an issue you found on one credit report, the action will be reflected on all the other reports.

Use the chart below to determine your credit tier, based on your credit score. Your credit score will drastically affect the interest rates you will be offered at the dealership or credit union:

| Super prime | 781-850 |

| Prime | 681-780 |

| Nonprime | 601-680 |

| Subprime | 501-600 |

| Deep subprime | 300-500 |

Here are the approximate interest rates you can expect in the nonprime to deep subprime markets. In general, you will see higher interest rates on used cars. New cars tend to have lower rates, but new cars obviously cost more.

New-Car Loan:

Nonprime: 7.1 percent

Subprime: 11.4 percent

Deep subprime: 14.1 percent

Used-Car Loan:

Nonprime: 10.4 percent

Subprime: 16.9 percent

Deep subprime: 19.8 percent

With a good idea of the rates you'll be offered, you can now start shopping.

2: Determine What You Can Afford

Most of us have a rough idea of what we can afford for a monthly car payment. But focusing too much on the monthly payment ignores the bigger picture. You need to save room in your budget for fuel and insurance costs, the latter of which tends to be more expensive if you have poor credit.

If you're on a tight monthly budget, shopping for a used car will likely make the most sense, even when factoring in the lower interest rates offered on new cars. When you look at car prices on the lot, it is important to understand how the bad-credit interest rates will affect the total cost of the auto loan and the monthly payment.

For example, if we use the average interest rate received by each group of borrowers with credit scores below 660, here's how those numbers work out in real life for a $17,000 used car with a 66-month auto loan:

- Nonprime: 10.4 percent APR = $340 per month

- Subprime: 16.9 percent APR = $398 per month

- Deep subprime: 19.8 percent APR = $425 per month

It's clear that if you're a deep subprime borrower looking for a $300 monthly payment, an auto loan for a $17,000 vehicle is more than you can handle. If you had your heart set on buying a car in that range, you'd either need to save up $5,000 to get your loan amount down to $12,000 — which, at 19.8 percent interest, amounts to a monthly payment of about $300 — or look for a less expensive vehicle.

"We love our leather seats and sunroofs," says Griffin, "but when your credit isn't stellar, it is better to look at a lower-end automobile."

Understanding this reality before you start shopping will do more than help you save time. It will also save you the frustration of looking at cars that don't fit your budget. If you're not sure how to figure out your price range, read "How Much Car Can I Afford?"

3: Get Your Financial Documents in Order

Before applying for your loan, have your paperwork in order. Lenders may need to see pay stubs or W-2 or 1099 forms to prove income. If you're in a line of work in which it's hard to prove income — if you're a restaurant server who has a lot of income in cash tips, for example — bring in bank statements that show a history of consistent cash deposits to your account. Some lenders will accept bank statements in place of, or in addition to, standard pay stubs.

The lender might want to see your name on a utility bill, rental agreement or mortgage statement that also shows your current address. Some banks may also accept cellphone bills. The lender wants to know where you live for a couple of reasons. First, it shows stability. A borrower who has lived at the same address for 10 years is likely to stay put, and banks like stability. The second reason is that the bank wants to know where to send the tow truck if the borrower stops paying and the vehicle needs to be repossessed.

Bring recent documents. The lender will likely want to see proof of residency and income that are no more than 30 days old. Having these documents in hand when you arrive at the dealership can mean getting a loan response in a few hours instead of a few days. In addition to documents, some lenders will ask for personal references. When requested, the lender will want names, phone numbers and addresses.

Pro tip: Bring a copy of your credit report with you to the dealership. Having it available might help the dealership skip running your credit, which it would need to do to give you a ballpark idea of the approval you'll be offered.

If you have a co-signer, have his or her information on hand, too.

4: Get Preapproved for an Auto Loan

Now it's time to get approved for a car loan. Make sure to seek approval from more than one lender. Because while your poor credit might bind you to a high-interest rate, some auto loan rates could still be better than others.

Many dealership websites have credit applications you can fill out online to get a preapproval. If you don't see the application on the front page, it may be under the "Finance" tab.

Also, check with your bank or credit union. It might be more willing to approve you since you already have an established financial relationship. You might also try an online lender such as Capital One, which offers auto loans for people with a credit score of 500 and up.

Don't worry that filling out too many loan applications will harm your credit.

"Lenders know you are searching for the best rate," Griffin says. As long as you apply for loans in a 14-day period, they will only count as one hard inquiry on your credit report.

For some shoppers, it may even be possible to get a loan approval without a hard inquiry.

5: Pick the Right Car

When it comes to deciding the car you're going to buy, it helps to understand that loan companies do not view all cars the same way. Imagine two $12,000 vehicles: The first is a 3-year-old economy car with 45,000 miles. The other is a 10-year-old luxury car with 120,000 miles. Although both cars have the same selling price, they are more likely to approve the newer car with fewer miles.

Loan companies use a complicated formula when deciding which cars to finance, and the criteria can vary among banks. The vehicle's age, mileage, history, and the buyer's credit history all play a role in the financing equation. So if you're approved for financing, you may have to pick a car that gets a lender's OK, and it might not be the one you had your eye on. Prepare to be flexible. Also, that high APR you're going to pay may sting, but remember that for many buyers who are rebuilding credit, it's temporary.

"Generally, if somebody has made good payments for 18 months, assuming the customer hasn't created new credit problems, then there may be an opportunity to get a lower interest rate," said Martin Less, president of Nationwide Acceptance, a lender that works with people in the nonprime market.

Once your credit is on better footing, you could refinance the loan at a lower rate with a different lender.

6: Make a Down Payment

Here is a hard truth about buying a car with relatively new or bad credit: You'll likely need a down payment. Most banks will require "at least 10 percent down payment, or $1,000, whichever is greater," Less says.

Using a trade-in as a down payment is a popular option, but some banks may prefer cash. In the eyes of some lenders, a cash down payment helps prove that you're committed to maintaining the auto loan.

As a rule, the more money you put down, either from cash or a trade-in, the better your chances will be of getting a fair approval.

7: Apply for the Loan and Close the Deal

If you had trouble getting preapproved, or prefer to handle it in person, head to a big-name car dealership. Most dealerships that do lots of business will have a system in place to help get approval for shoppers who have less than perfect credit. In some cases, dealerships will even have dedicated personnel whose job is getting subprime and deep subprime loans approved. This group is often called the special finance department.

Dealerships that regularly work with credit-challenged shoppers will know which lender will be most likely to approve your loan based on your specific situation. Just as all buyers don't have the same level of bad credit, not all lenders have the same requirements. A dealer might need to place a buyer with a recent bankruptcy with a different bank than one he'd select for a buyer who has a low score because of a recent divorce. A dealer who knows where to send a loan can be key in getting a shopper approved.

Pro tip: Don't be afraid to shop around for auto loans. Often, shoppers with bad credit will jump on the first deal for which they are approved, no matter how unappealing it seems. That's understandable, especially if you've been turned down a few times in the past. But just because you've gotten an approval doesn't mean you have to sign a contract that makes you feel uneasy. If the deal you're offered doesn't sit right with you, keep looking. The reality is that if one dealership can get you approved, chances are good another dealer can, too.

Having poor credit doesn't mean you're stuck with a bad deal, can't negotiate or can't shop for the car that's best for you.

8: Keep the Loan in Good Standing

Make your payments on time. When possible, consider making additional, or larger, payments on your auto loan. Those additional payments will look good on your credit report, make you look good in the eyes of the lender, and save you money in interest while you have the loan. Also doing so will set you up for better terms when it is time to get your next car.

And if you run into trouble while paying the loan, don't hide from the situation. Tell the finance company immediately. Some lenders will allow you to make small payments for a time, adding the remaining balance to the end of the loan. If the situation is dire, a bank may even allow you to miss a payment or two while things get better.

"The most important thing [borrowers] can do is keep communications going," Less says. "Let the lender know what the circumstances are, and lenders will generally work with the customers through temporary problems."

9: Resist the Urge to Trade Up

A number of new-car dealerships offer their credit-challenged customers the chance to trade into another vehicle without a significant increase in their monthly payment provided they've made a year's worth of consecutive on-time payments. While it may be tempting to get out of a Nissan Versa and into a Nissan Altima, for example, you will be adding more debt to your next loan.

If you want to move up to a larger or nicer car, a smarter strategy is to refinance the current loan for a lower interest rate and monthly payment, then stick with the loan until there is some equity or the initial car is paid off. When it's time to purchase your next car, you should be in a higher credit tier — assuming you've also done well on your other bills — and will qualify for a nicer car.

The New You

If you've done your credit homework, shopped within your price range and made all your payments, you've not only improved your bad credit but also set up positive finance habits that will serve you well for years to come.