Drive by Numbers - A Tale of Two Marches

March 2009 was depressing. I'm not talking about my personal life here, but as someone who looks at auto industry numbers on a daily basis, there was not a lot to rejoice in. Incentives were at an all-time high, inventories were ridiculously large, and bankruptcies were a part of our daily vernacular. We were in a scary place and I'm getting glum just thinking about it. But, I'm looking at numbers from last month in my 17.5MB spreadsheet and I'm noticing what a HUGE difference three years makes. Although I'm not ready to pop the cork off my bottle of Ace of Spades yet, I may be ready to serve the Veuve Clicquot. We sold more vehicles last month than in any month since August 2007, and the all around metrics in which we judge the health of the auto industry have shown a drastic improvement.

March 2009 was depressing. I'm not talking about my personal life here, but as someone who looks at auto industry numbers on a daily basis, there was not a lot to rejoice in. Incentives were at an all-time high, inventories were ridiculously large, and bankruptcies were a part of our daily vernacular. We were in a scary place and I'm getting glum just thinking about it. But, I'm looking at numbers from last month in my 17.5MB spreadsheet and I'm noticing what a HUGE difference three years makes. Although I'm not ready to pop the cork off my bottle of Ace of Spades yet, I may be ready to serve the Veuve Clicquot. We sold more vehicles last month than in any month since August 2007, and the all around metrics in which we judge the health of the auto industry have shown a drastic improvement.

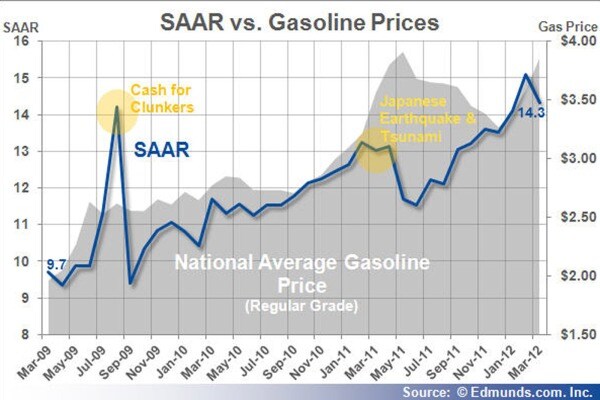

9.7 vs. 14.3

March 2009:

When we calculated the Seasonally Adjusted Annual Rate (SAAR) for new vehicles in March 2009 to be 9.7M, I felt slightly optimistic. It was better than the 9.2M we saw the month prior, but it still hurt. It hurt bad. At that point, every month so far in 2009 had a SAAR in the 9M range and as frightening as this was, we weren't even remotely out of the woods. In fact, we had three more months ahead of us that would witness sales in the 9M SAAR range. Cash for Clunkers came along that summer, which temporary pulled us out the doldrums, but it was followed by a bitter payback period that fall. In total, 2009 had seven months with a sub 10M SAAR. The last time that happened was 1967.

March 2012:

It was hard to top the elation we felt when February came in with a SAAR at 15.1M, but the industry wasn't disappointed with March's 14.3M either. It's tough to have a strong SAAR in March since high sales are expected and SAAR's equation is meant to depress the number rather than boost it. Truth be told, I thought the sales could be higher, but there were a few automakers that didn't finish as strongly as anticipated. Compared to March 2009, however, the difference is extreme - car sales were up 64% in terms of raw units sold. Looking at individual brand performance for these two months, VW and Kia were up the most, selling 133% more cars than they did back in March 2009. On the other side of the spectrum, Suzuki, Smart, and Saab all sold fewer vehicles than they did three years ago. If not for Subaru, I'd say car brands that start with the letter "S" are cursed. Remember Saturn?

$3,137 vs. $2,118

March 2009:

Once upon a time, auto companies needed very little in the way of monetary incentive in order to sell cars. Clearly, that is no longer the case. But there was never a time when more money was needed than in March 2009. Edmunds.com calculates automaker incentive spending in our True Cost of Incentives (TCI) number, and that month it nearly took my breath away. The industry average crossed the $3,000 threshold for the first time with an average spend being $3,137 per vehicle. Chrysler led all companies with an average spend of $4,872 per vehicle. And if you took their incentives as a percentage of selling price, you were looking at a discount rate in excess of 20%. Ford and GM were not far behind. Even current industry darling, Hyundai had a discount rate of 18.5%. Oh, how times have changed.

March 2012:

On average, automakers spent $2,118 per new vehicle in March 2012. The TCI has fallen a much needed 32% when you do the March '09 vs. March '12 comparison. The cash spent on finance subsidies has gone down 37%, and now that leasing is a more popular option throughout the industry, more money is spent on lease subvention. I spend a fair amount of time looking at incentives data and I'm constantly asked if it's a consumer friendly market out there. It is, but gone are the days of the once-in-a-lifetime deals (remember the buy one truck, get a car free deal some Chrysler dealers ran?) With current sales pacing on the strong side and production levels set for conservative sales targets, it doesn't look like there is any immediate need for those deals to come back.

97 vs. 53

March 2009:

It is hard to lower inventories when you can't sell cars. And in March of 2009, new car inventories were ballooning. Along with raw inventory, days' supply, I also like to look at a measure called days-to-turn, which measures how long a vehicle has sat on a dealer lot before being sold. When there are not a lot of buyers out there, this number can get frightening. Days-to-turn hit a near record in March of 2009 with the average vehicle taking 97 days to sell. It was scary to think that, on average, a car sat on a lot for more than three months before finding an owner. Bad for automakers, bad for dealers. The actual record high happened two months later in May 2009 at 98 days, but it's pretty much all the same — bad. Large cars (the segment in which the Impala and Avalon compete in) sat on dealer lots an average of 126 days before sold. Even the popular midsized sedan segment had an average of 104 days. Dark days indeed.

March 2012:

Inventory has taken a very different turn in the past year. It was just last March when Japan was struck with the earthquake and tsunami which crippled Japanese factories and supply chains. The effect was felt throughout the industry and days-to-turn numbers were at sustained lows through the fall. At 53 days in March and February of this year, it's higher than it has been in recent months but shockingly different than the 97 days we witnessed back in 2009 — a 45% decline. The Toyota Prius c, the focus of one of my previous columns, had the lowest days-to-turn in the industry at 8 days. Before the great recession, a days-to-turn of 60 days was considered healthy.

21

Of course, it's easy to say the auto industry is a vastly different place than it was back in 2009. I don't think that's a shocking concept to anyone. After all, the world is a different place. But, looking at the raw numbers is a good reminder of just how far we've come. On the wall of my 7th grade history class was the George Santayana quote "Those who cannot remember the past are condemned to repeat it." It's a good sentiment because our past is something that can get lost in the shuffle of the positive recovery news. But, enough with the heavy subject matter; I'm off to Las Vegas for the weekend. I know as a numbers person the odds are against me (and I'm choosing to ignore the past here), but nothing beats the thrill of adding your cards up to 21. I'll report my winnings - or losses - next week.

Do you like numbers too? If so, check out our Industry Data Center

Jessica Caldwell is the Senior Director of Pricing & Industry Analysis for Edmunds.com. Follow @jessrcaldwell on Twitter.