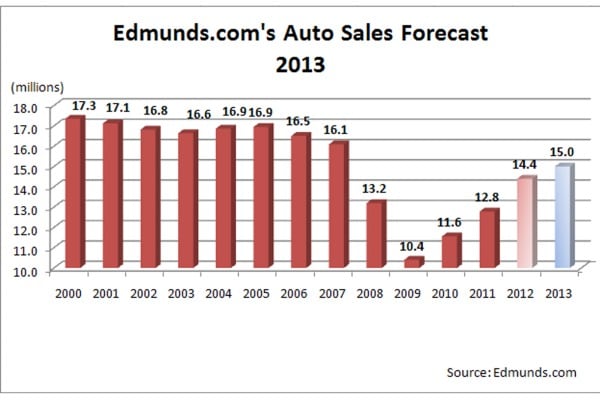

Edmunds.com 2013 Auto Sales Forecast: 15 Million

Auto sales growth will continue in 2013, although at a slower rate than in recent years. Edmunds.com forecasts sales of 15 million light vehicles in 2013, an increase of 4 percent over the 14.4 million expected in 2012. This would make 2013 the first year of non-double-digit sales growth since the recovery began. Economic uncertainty due to unresolved fiscal issues at home and (actual and feared) spillover effects from slowing economies abroad will continue to slow the pace of American economic growth, including car sales. But many of the same factors in play now will still support car sales momentum in 2013. The release of pent-up demand from buyers who deferred sales during the recession will intensify as credit conditions further loosen and the increasingly aged fleet drives more consumers back to the new car market. Importantly, sales will receive a boost in 2013 from an expected nearly 500,000 additional lease returners compared to 2012, who will lease or buy a new vehicle when their current leases terminate.

More Sales Per Driver Expected

Edmunds.com's forecast assumes that the rate of new car sales per licensed driver will continue to increase as it has each year since hitting a recession low of 0.05 in 2009. This rate is expected to be 0.067 in 2012 and 0.0695 in 2013. Even after 4 years of growth, sales per driver will remain substantially below its yearly average of 0.086 from 1999-2007. However, new car sales (and thus sales per driver) were likely inflated during that period because consumers spent more freely due to the wealth effects of the housing price bubble and the stock market bubble.

Prior to these "bubble years," annual sales per driver averaged 0.083 from 1993-98. The driver population is larger now than in the mid-1990s, having increased by 2 million drivers per year on average since 1991. But, while nearly 20 years of quality improvements have undoubtedly led to less frequent vehicle replacement, there is likely room for the rate of sales per driver to grow beyond 0.0695. Leasing is more readily available now, which can lead to more frequent replacement. And the rate of 0.0695 assumes conservative growth given that sales per driver have increased 10 percent per year on average during the recovery. (Growth of 10 percent in 2013 would result in a rate of sales per driver of 0.074, or 16.1 million auto sales.)

Influx of Lease Returners to Create a Sales Surge

A key reason that sales will increase at a faster rate than drivers in 2013 is that substantially more car leases will terminate in 2013 than in 2012, increasing the pool of likely buyers. The growth in lease returners reflects the slowdown in leasing during the recession that bottomed out in 2009, resulting in many fewer lessees available to return to market in 2012. The revival of leasing since 2010 should noticeably impact new car sales in 2013. Assuming that 70 percent of 2010 leases were 3-year leases and 30 percent of 2011 leases were 2-year leases and that 75 percent of lease expirations result in the lease or purchase of a new car, then 484,000 more lessees will return to the market in 2013 than in 2012.

Release of Pent-Up Demand: Still Going Strong

The greater number of sales from lease returners will add strong support to auto sales in 2013. Edmunds.com expects other factors to contribute as well. In particular, the release of pent-up demand from buyers who deferred sales during the recession will not only continue in 2013, but will likely do so at a higher rate than in 2012. One source that could draw more consumers back to the market is the increasingly aging fleet — the average age of vehicles in operation reached 11 years in the first quarter of 2012, according to Experian, despite an increase in vehicle trade-in age this year. Another source could be a more favorable pricing environment. With all of the top automakers generally healthy and looking to grow, the potential for supply to outpace demand and lead to lower net prices for consumers is high.

Greater access to credit also could spur a greater release of pent-up demand in 2013. After severely contracting during the recession, credit began expanding in the first half of 2010. The share of subprime new car loans returned to pre-recession levels in the second quarter of 2012. While the return of subprime lending could suggest a slowdown in the expansion of credit, the Federal Reserve's new open-ended asset-buying plan is intended to keep banks flush with cash and thus willing to increase lending. Even though the main target of the Fed's plan is mortgage lending, auto loan borrowers could benefit from spillover effects. Plus, the actual number of subprime loans is still below 2007 levels due to the current lower level of sales, raising the possibility of continued growth — although the fallout from the subprime bubble makes it unlikely that subprime borrowers will regain access to credit markets to the same extent as during the bubble. There is also room for credit expansion in the prime segment — recent Edmunds.com data showed that more consumers are getting auto loans with zero percent APRs, a trend that could bring out more buyers if it continues in 2013.

The Sales Growth Slowdown

Although the above factors will support auto sales in 2013, Edmunds.com expects auto sales to grow at a slower pace next year because, quite simply, economic uncertainty continues and risk to the economy abounds. Even though the Fed's recently updated forecasts for 2013 GDP and unemployment both showed improvement, the global situation remains precarious. While numerous analysts are currently more optimistic following the launch of the Fed's plan and a similar one from the European Central Bank both aimed at triggering growth by promoting investment and spending, it remains unclear whether such plans will actually work as intended; in fact, the success of previous plans has been much debated. The potential for the economic recovery to remain sluggish in 2013 cannot be ignored and as a result, the downside risk to auto sales growth remains significant.

Lacey Plache is the Chief Economist for Edmunds.com. Follow @AutoEconomist on Twitter.